World

World’s poorest countries pushed to brink of collapse under China debt

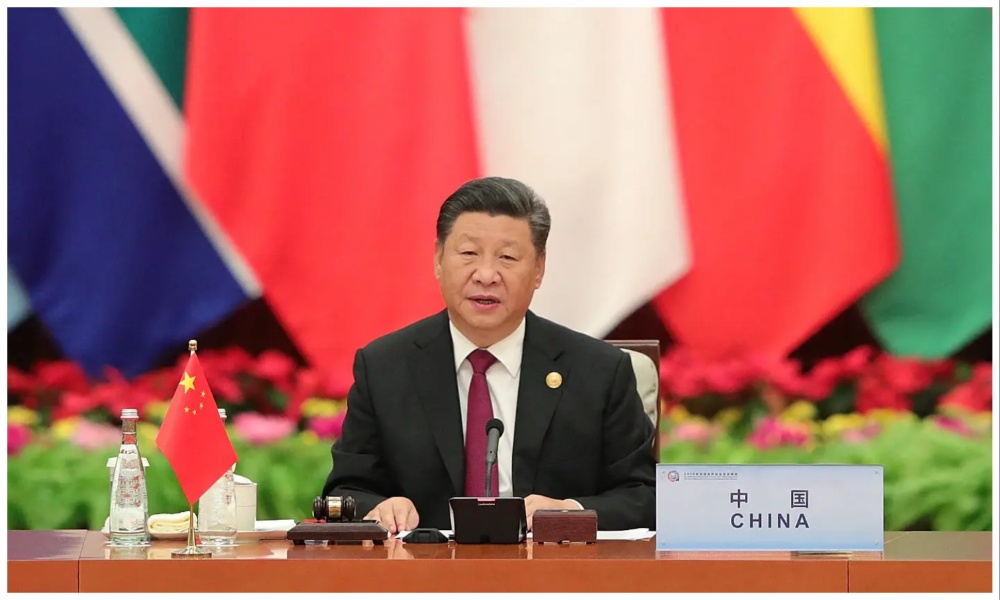

At least a dozen poor countries are buckling under the weight of hundreds of billions of dollars in debt, most of which is owed to China.

A recent analysis, carried out by the Associated Press, found that for a dozen countries, paying back their debt is consuming a growing amount of their tax revenue needed to keep basic services going.

Among the countries analyzed was Pakistan, Kenya, Zambia, Laos and Mongolia and it was found that paying back their debt is also draining foreign currency reserves that these countries use to pay interest on the loans – leaving some with just months before that money is gone.

AP reported that behind the scenes is China’s reluctance to forgive debt and its extreme secrecy about how much money it has loaned and on what terms, which has kept other major lenders from stepping in to help.

According to World Bank data analyzed by Statista recently, countries heavily in debt to China are mostly located in Africa, but can also be found in Central Asia, Southeast Asia and the Pacific.

And, Statista reports that the new Belt and Road Initiative, which finances the construction of port, rail and land infrastructure, has created much debt to China for participating countries, specifically poor countries.

As of March last year, 215 cooperation documents had been signed with 149 countries on the initiative.

Countries in AP’s analysis meanwhile had as much as 50% of their foreign loans from China and most were devoting more than a third of government revenue to paying off foreign debt.

Two of them, Zambia and Sri Lanka, have already gone into default, unable to make even interest payments on loans financing the construction of ports, mines and power plants.

In Pakistan, millions of textile workers have been laid off because the country has too much foreign debt and can’t afford to keep the electricity on and machines running, AP stated.

In Kenya, the government has held back paychecks to thousands of civil service workers to save cash to pay foreign loans. The president’s chief economic adviser tweeted last month, “Salaries or default? Take your pick.”

The study also found that since Sri Lanka defaulted a year ago, a half-million industrial jobs have vanished, inflation has risen by 50% and more than half the population in many parts of the country has fallen into poverty.

The study found that experts predict that unless China begins to soften its stance on its loans to poor countries, there could be a wave of more defaults and political upheavals.

AP’s report stated that a case study of how it has played out is in Zambia, a landlocked country of 20 million people in southern Africa that over the past two decades has borrowed billions of dollars from Chinese state-owned banks to build dams, railways and roads.

While the loans boosted Zambia’s economy, they also raised foreign interest payments so high that there was little left for the government, forcing it to cut spending on healthcare, social services and subsidies to farmers for seed and fertilizer.

In the past under such circumstances, big government lenders such as the U.S., Japan and France would work out deals to forgive some debt, with each lender disclosing clearly what they were owed and on what terms so no one would feel cheated.

But China didn’t play by those rules, AP reported. It refused at first to even join in multinational talks, negotiating separately with Zambia and insisting on confidentiality that barred the country from telling non-Chinese lenders the terms of the loans.

By late 2020, Zambia was unable to pay the interest and defaulted, setting off a cycle of spending cuts and deepening poverty.

Since then, inflation in Zambia has increased by 50%, unemployment has hit a 17-year high and the nation’s currency, the kwacha, has lost 30% of its value in just seven months. AP also found that 3.5 million Zambians are now not getting enough food.

AP reported that a few months after Zambia defaulted, researchers found that the country owed $6.6 billion to Chinese state-owned banks, double what many thought at the time and about a third of the country’s total debt.

China’s unwillingness however to take big losses on the hundreds of billions of dollars it is owed, as the International Monetary Fund and World Bank have urged, has left many countries on a treadmill of paying back interest, which stifles the economic growth that would help them pay off the debt.

For Pakistan, its foreign cash reserves have plunged more than 50%, according to AP’s analysis, while in nine of the 12 countries analyzed, foreign cash reserves have dropped on average of 25% in just one year.

Based on this, Pakistan for example has only two months left of foreign cash to pay for food, fuel and other essential imports if it does not get a bailout. Other countries, such as Mongolia, have eight months left.

AP found that last month, Pakistan was so desperate to prevent more blackouts that it struck a deal to buy discounted oil from Russia, breaking ranks with the US-led effort to shut off Vladimir Putin’s funds.

In Sri Lanka, rioters poured into the streets last July, setting homes of government ministers aflame and storming the presidential palace, sending the leader tied to onerous deals with China fleeing the country.

China has however disputed the idea that Beijing is an unforgiving lender and said in a statement that the Federal Reserve was to blame.

It said that if it is to accede to IMF and World Bank demands to forgive a portion of its loans, so should multilateral lenders, which it views as US proxies.

“We call on these institutions to actively participate in relevant actions in accordance with the principle of ‘joint action, fair burden’ and make greater contributions to help developing countries tide over the difficulties,” the statement said.

But China’s approach to lending is widely considered more transactional and criticized as “opaque” and analysts see Beijing’s desire to access oil, minerals and other commodities as the driving force behind Chinese lenders being less prone to applying strict conditions in helping governments finance roads, bridges and railroads – so as to unlock those resources.

Just last month, US Treasury Secretary Janet Yellen told lawmakers: “I’m very, very concerned about some of the activities that China engages in globally, investing in countries in ways that leave them trapped in debt and don’t promote economic development.”

“We are working very hard to counter that influence in all of the international institutions that we participate in,” she said.

Since 2017, China has become the world’s largest official creditor, surpassing the World Bank, IMF and 22-member Paris Club combined, Brent Neiman, a counselor to Yellen, said late last year.

Politico meanwhile reported earlier this month that China’s financing of projects in other countries between 2000 and 2017 totaled more than $800 billion, most of that in the form of loans.

But for some poor countries struggling to repay China, they now find themselves stuck in a kind of loan limbo: China won’t budge in taking losses, and the IMF won’t offer low-interest loans if the money is just going to pay interest on Chinese debt.

World

Venezuela earthquake death toll nears 1,500 as race to find survivors intensifies

The powerful magnitude 7.2 and 7.5 earthquakes struck on Wednesday, devastating the coastal state of La Guaira, about 40 kilometres north of Caracas.

The death toll from Venezuela’s devastating twin earthquakes has climbed to nearly 1,500 as rescue teams continue searching for survivors trapped beneath collapsed buildings, with authorities warning that time is running out.

The powerful magnitude 7.2 and 7.5 earthquakes struck on Wednesday, devastating the coastal state of La Guaira, about 40 kilometres north of Caracas. Officials say the disaster has left more than 3,100 people injured, displaced over 12,700 residents and destroyed at least 774 buildings.

Acting President Delcy Rodríguez said rescue operations would continue after emergency crews recovered additional survivors on Sunday.

“Rescue and recovery efforts are ongoing. Today we have recovered people alive, and therefore operations are not being suspended. We always maintain hope,” she said.

Rodríguez also announced the formation of a presidential commission to assess the structural safety of damaged buildings, extended the suspension of school classes for another week and said electricity had been restored to around 75 percent of La Guaira.

More than 2,600 international rescue workers have joined Venezuelan emergency teams, searching through mountains of rubble with the help of specialised equipment and rescue dogs. Several survivors, including children, have been pulled alive from collapsed buildings in recent days.

Among the latest rescues were an infant freed by US rescue personnel, an 11-year-old boy rescued by Colombian teams after being trapped three metres beneath rubble, and another 11-year-old saved by Mexican crews. Officials say such rescues are becoming increasingly rare as the critical 72-hour survival window passes.

Swiss rescue team leader Sebastian Eugster said the chances of finding survivors decrease significantly after the first three days.

“There exists a window of roughly 72 hours where the probability of rescuing people alive is much higher,” he said.

Authorities say nearly 50,000 people remain unaccounted for, although that figure is based largely on reports submitted through an opposition-backed missing persons website and has not been independently verified.

The United States Geological Survey has warned the final death toll could exceed 10,000, potentially making the disaster one of the deadliest earthquakes in Latin America in the past century.

The catastrophe has also disrupted the country’s energy sector. Venezuela’s largest oil refinery, the 645,000-barrel-per-day Amuay refinery, suspended operations following a major power outage in western Falcón state.

International aid continues to arrive, with the United States expected to announce an additional humanitarian assistance package worth hundreds of millions of dollars, on top of the $150 million already pledged.

The earthquakes have struck Venezuela at a time of ongoing political and economic instability, further complicating relief efforts as authorities, volunteers and international rescue teams continue the search for survivors.

A helicopter belonging to Saudi oil giant Aramco crashed on Sunday in Ras Tanura on Saudi Arabia’s eastern coast on the Gulf, west of the Strait of Hormuz, killing 14 nationals, the state news agency reported, adding that the cause was unknown.

Aramco had resumed crude oil loadings on Friday at its Ras Tanura terminal in the Gulf after they were halted for nearly four months, Reuters reported.

“The relevant authorities have launched a full investigation to determine the cause of the crash,” the state news agency added.

Aramco did not respond immediately to an emailed request for comment.

The incident took place at 6 a.m. local time (0300 GMT), the state agency said, without providing further details.

Saudi Arabia, the world’s biggest oil exporter, has joined a rush to move cargoes after Middle East producers ramped up oil and gas output and exports ahead of an interim deal to halt the war between the United States and Iran.

World

Israel, Lebanon sign initial agreement after US-mediated talks

Israeli Prime Minister Benjamin Netanyahu said the agreement allows Israeli forces to continue to occupy southern Lebanon if Hezbollah does not disarm.

Israel and Lebanon signed a framework agreement in Washington on Friday following several days of talks to secure an end to fighting between Israel and Iran-backed Hezbollahmilitants, though both sides framed the deal as an initial step, Reuters reported.

Lebanese Ambassador Nada Moawad and her Israeli counterpart Yechiel Leiter signed the trilateral document with the U.S. at the State Department in Washington, providing few details.

Israeli Prime Minister Benjamin Netanyahu said the agreement allows Israeli forces to continue to occupy southern Lebanon if Hezbollah does not disarm.

“Today we’ve taken the first step in what will be a difficult journey, without a doubt, but an important and an essential and a necessary one,” U.S. Secretary of State Marco Rubio said before the agreement was inked.

In a later statement he said that the U.S. would facilitate the implementation of the deal through a trilateral “Military Coordination Group for Lebanon” and that Washington would commit significant resources, including an immediate $100 million in humanitarian assistance in coordination with the U.N.

Rubio added that the U.S. reaffirmed its intent to improve the capabilities of the Lebanese Armed Forces “to more effectively establish sovereignty throughout Lebanese territory” with more than $30 million in funds under existing U.S. authorities and appropriations.

The conflict between Israel and Hezbollah broke out when the armed group fired at Israel on March 2, days after the U.S. and Israel attacked Iran. The Hezbollah attacks triggered Israeli air and ground attacks that have killed more than 4,000 people in Lebanon and displaced more than a million.

Lebanon’s Moawad also called it a “first step” on the road to restoring Lebanese sovereignty.

“Iran is out, Hezbollah is out, and the road to peace between Israel and Lebanon is in,” Leiter said.

Netanyahu said in a statement that the deal would also allow the Lebanese army “to begin organizing to take control of territory,” starting with what he described as two “pilot zones” from which Israeli troops would withdraw from land they occupied during the war.

Israel describes that territory as a “security zone” or “buffer zone” where its troops can thwart Hezbollah attacks on northern Israel.

Lebanese President Joseph Aoun said the agreement should allow Lebanese to return to “fully liberated” land and rebuilt homes with “no partner” in its sovereignty.

Israel’s death toll from this round of hostilities with Hezbollah includes at least 32 soldiers and four Israeli civilians. Hezbollah does not release figures on its war dead. Reuters reported on May 4 that several thousand Hezbollah fighters had been killed in the war.

A State Department official told Reuters on Thursday that Israel had agreed to pull back from some of the territory it has occupied, something Israeli and Lebanese officials denied.

Before the talks resumed this week, Israel and Hezbollah agreed to halt fire even as Israel kept troops in southern Lebanon.

Violence has persisted since the ceasefire, with Israel saying on Friday its troops had struck and killed what the military described as seven Hezbollah members who were operating near the territory it is occupying. Reuters could not confirm this.

“To the degree that the Lebanese army performs in dismantling and disarming Hezbollah, we will proceed with additional pilot zones and the ultimate determination of an internationally recognized, secure, and agreed upon border,” Leiter told reporters after the signing.

Hezbollah lawmaker Hassan Fadlallah said Lebanese authorities would not be able to enforce the agreement unless, with U.S. support, “they go to civil war,” pro-Iranian broadcaster Al Mayadeen reported, read the report.

Hezbollah would confront any measure taken by Lebanese authorities and would hold on to its weapons even more, adding that the group’s opposition was “serious” and would not allow authorities to implement their commitments on the ground, Fadlallah said.

Israeli forces dropped leaflets over the southern Lebanese town of Mansouri on Friday ordering residents to leave, Lebanese state media reported, the first such order issued since the latest ceasefire between Israel and Hezbollah took effect.

A senior Lebanese military official said Israel had recently added Mansouri to its occupation zone. The official said Lebanese farmers had continued to enter and leave the town, but had not been living there.

An Israeli military spokesperson said the military issued what it described as a “reminder” to the civilian population that “the area is within the security zone in which (Israeli) soldiers operate. It’s a reminder not to be in the area so they won’t be harmed.”

Tahawol: Pakistan’s attacks on civilians in Afghanistan

Saar: Pakistani airstrikes on Afghanistan

Pakistan orders undocumented Afghan nationals to leave by July 10

UNAMA confirms death of 28 civilians following Pakistani airstrikes on eastern Afghanistan

Afghanistan summons Pakistani diplomat over airspace violations and civilian bombing

Norway’s Viking-inspired World Cup team photo goes viral

TAPI project advances in Afghanistan as 84kms of pipeline laid

Afghanistan’s trade with Central Asia records sharp growth

Afghanistan to play in Diamond Jubilee Tournament opener against Maldives

Gaikwad set to replace injured Kohli for Afghanistan ODI Series

Tahawol: Pakistan’s attacks on civilians in Afghanistan

Saar: Pakistani airstrikes on Afghanistan

Tahawol: Calls for diplomacy between Kabul, Islamabad

Saar: US and Iran exchanging attacks

Saar: Concerns over Afghan deportations from Europe discussed

-

Latest News4 days ago

Latest News4 days agoTAPI project sees rapid progress in Afghanistan

-

Business2 days ago

Business2 days agoAfghanistan eyes direct Basmati rice imports from India amid tensions with Pakistan

-

International Sports3 days ago

International Sports3 days agoFIFA World Cup: Iran held by Egypt after controversial late goal Is disallowed

-

Latest News3 days ago

Latest News3 days agoDelawar says Afghanistan has achieved security and unity after 47 years

-

International Sports5 days ago

International Sports5 days agoFIFA World Cup: Messi turns 39, shows no signs of stopping

-

Latest News3 days ago

Latest News3 days agoEU announces major funding to support Afghan small businesses

-

Latest News4 days ago

Latest News4 days agoAshura observed across Afghanistan with calls for unity and justice

-

Latest News5 days ago

Latest News5 days agoAfghanistan ranks last in KidsRights Index 2026